There are, and this is not an exaggeration, thousands of new satellites being launched into space in the coming years, many of them set to provide additional connectivity to shipping and the ocean industries.

Technological developments have meant that satellites are getting smaller, and therefore cheaper and quicker to build and launch, which has led to a handful of private companies being launched with wealthy backing to make the most of what they see as a gap in the connectivity market(it may be cheaper but it is far from cheap).

Companies such as OneWeb (with Virgin’s Sir Richard Branson support) , SpaceX (Elon Musk) and Swarm Technologies have ambitions to push a large number of satellites into what is known as a low earth orbit to offer high speed broadband connectivity.

Other companies launching satellites Hiber, Capella Space and Planet, though these are not necessarily targeting maritime, ocean or shipping with broadband/communication solutions.

US-founded, but now London-based, OneWeb is on track to have 650 satellites in orbit and operational by late next year as it challenges existing satellite communication provider, including maritime. It’s first launch was in February 2019 when it sent up six satellites to meet its regulatory requirements and secure its requested frequencies. Last month it sent up a further 34 of its fridge sized satellites in one single launch, all set to go into low earth orbit, and the remaining will be launched in a rapid launch schedule in the coming year.

OneWeb, which was launched in 2012 as WorldVu Satellites Limited and with backing from Sir Richard Branson when it launched in 2012. It has also secured $1bn in backing from Softbank. Its aim is to create ubiquitous broadband connectivity globally, with speeds that equal terrestrial broadband capabilities. But while its headline mission has been to give aces to remote places in the world, it has identified a market opportunity out at sea.

Carole Plessy is OneWeb’s head of commercial product development. She joined the company in late 2018 after nearly 20 years at Inmarsat where she was heavily involved in its maritime and digitalisation product developments. Plessy says there is a definite gap in the maritime market that OneWeb seeks to plug with its satellite service.

Despite an existing abundance of service providers, both in the VSAT and L-band spectrum, there is a need for satellite broadband speeds that match the service that ground based telecom service providers offer, she says, and at a much lower price and abundance than can be offered today.

This is important, she adds, given that companies like Kongsberg, Wärtsilä, ABB, shipyards and other service providers seek to offer maintenance and software packages with ubiquitous connectivity, in addition to hardware.

“I’m reluctant to see ourselves as a VSAT solution provider,” she adds, promising that the company’s service will have lower latency (i.e. faster real time connection), high data throughput but at a fraction of the cost. “That’s where OneWeb’s DNA is -benchmarked with terrestrial connectivity.”

Plessy says that poor latency and restricted bandwidth of existing satellite connectivity means that ship managers, asset operators and other companies with remote systems, have needed to use bespoke, and therefore expensive, communication systems and services. By offering global satellite connectivity that mirrors terrestrial broadband speeds, one can then let remote connections use off-the-shelf systems such as Microsoft 365 and other standard communication tools.

Changing Markets

While OneWeb is targeting the ocean industries – oil & gas, energy and maritime – it still uses an indirect route to market, the same service providers that companies like Iridium and Inmarsat utilize too. The company is also selling to telecoms companies which are also increasing their presence in the industrial sector. The Telecom giant Orange, for example, is active in the oil and gas sector.

One of the reasons for this cautious step into the market, says Plessy – who with her long career at Inmarsat has gained a strong feel for the maritime industry – are the layers of regulation and requirements that are in place to secure (safety related) radio telephony and satellite access to the assets and their crews. But in the end, the objective, once those regulations are met, is to treat the vessel as a remote fully integrated office, and to allow for the data flows to ensure asset data is available.

This she says will be especially important as one sees how technology companies have evolved their offerings from being product based to be service orientated.

The demand for high speed connectivity, and competitive costs is of course changing the satellite communication landscape. OneWeb has signed a Memorandum of Understanding with US satellite service provider Iridium, and Plessy thinks this will be a great help in the future, particularly as Iridium now has permission to provide the ship safety service GMDSS which used to be the sole responsibility of Inmarsat.

Small and mighty: Swarm

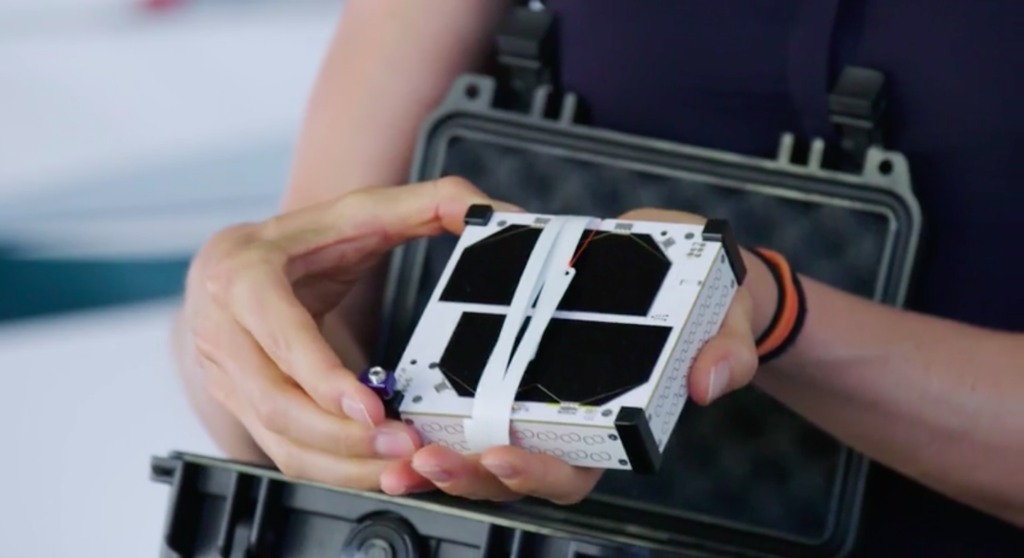

While OneWeb’s satellites are the size of a small fridge, another satellite fledgling company Swarm Technologies is launching satellites about the Size of an Ipad.

Co-founder and Chief Technology Officer Benjamin Longmier says the intention is to get 150 of these satellites into space in the next year, in batches of 12 to 24 per rocket launch. The company currently has nine in orbit. While Swarm is focusing on the scientific communities, Longmeir confirmed that his company has a good base of customer interest for ocean applications.

A year ago Swarm raised $25m to build what it called at the time the lowest cost satellite network. At the time the company listed shipping containers and asset tracking across the oceans as one of it target applications.

Mergers, acquisitions, de-listings and change

There will be other changes. Inmarsat’s delisting from the London Stock Exchange following a buyout by a consortium of corporate investors, will be for a very good reason given the company’s financial performance ahead of the delisting and the development of its services.

In the announcement regarding the takeover in March 2019 the consortium explained its reasoning for the offer.“Triton Bidco believes that integrated satellite operators with scale like Inmarsat are well positioned as network provision becomes more complex. While Inmarsat’s end markets, notably maritime and government, are competitive, Triton Bidco believes Inmarsat is well positioned for growth based on its unique global infrastructure, leading technological and capacity roadmap and strong spectrum holdings. In particular, Triton Bidco believes that Inmarsat’s business model is characterised by predictable revenues from a range of long-term contracts with governments and other financially secure customers.”

Another British technology group, Cobham, which has a division offering satellite connectivity services, has also recently delisted from the London Stock Exchange following a take over by equity group Advent International in January 2020.

Whether this leads to further mergers and consolidation remains to be seen. Inmarsat acquired Stratos in 2009.

Oneweb’s Carole Plessy thinks there will be more links, collaboration between companies offering L-Band services (which are in a mid-earth geostationary orbits a lot further away from earth) and the newcomers.

The growth of digitalisation could become very visible by 2024 in the night sky. Most of the new satellites being launched in the next four years are low earth orbit (LEO) satellites. LEO generally means a satellite at an altitude of between 500km to about 2,000 km above sea level, and the number of satellites is impressive.

By 2024, if the claims of the manufacturers are accurate, there could be over 40,000. Many of these new LEO satellites could well be visible to the naked eye. So to put this into perspective, astronomers a decade or so ago counted only 9,110 stars that are visible to the naked eye (magnitude 6.5) on a dark clear night across both hemispheres.

(Magnitude values are actually in reverse to how one might think, so the sun is -27 and the moon is -12-6. The brightest star in the sky, Sirius, a favourite star for mariners trained in celestial navigation is -1.6, and the naked eye limit is about +3 in a built up area with a lot of light pollution and about +6 otherwise. NOAA claims its satellites in LEO are 5.5 and visible)

This means that the 4,555 stars visible in either hemisphere could be swamped by thousands of new satellites, although the smaller they become the less visible to the naked eye they will likely be.

Naming the stars and classic Greek named constellations in the sky could be replaced by watching the moving white dots of satellites passing over our heads.