Press Release: Fuel cells could play an important role in the future of power generation, enabling the transition from traditional hydrocarbon fuels to low or zero-emission fuels. The fuel flexibility of solid oxide fuel cells (SOFC) offers a competitive advantage over the currently dominant proton exchange membrane fuel cell (PEMFC), which is limited to operating on hydrogen. Despite the hype of the hydrogen economy, it could be considered foolish to expect that an imminent abundant supply of green or blue high-purity hydrogen will become available to fulfill all demand in the near future, presenting an opportunity for the fuel agnostic SOFC.

The new IDTechEx report, “Solid Oxide Fuel Cells 2023-2033: Technology, Applications and Market Forecasts“, provides a comprehensive overview of the solid oxide fuel cell market, including an assessment of the key technology trends, major players and also includes granular 10-year market forecasts for solid oxide fuel cell demand (MW) and market value (US$), segmented by application areas. Overall, IDTechEx projects the market value to reach US$6.8 billion by 2033.

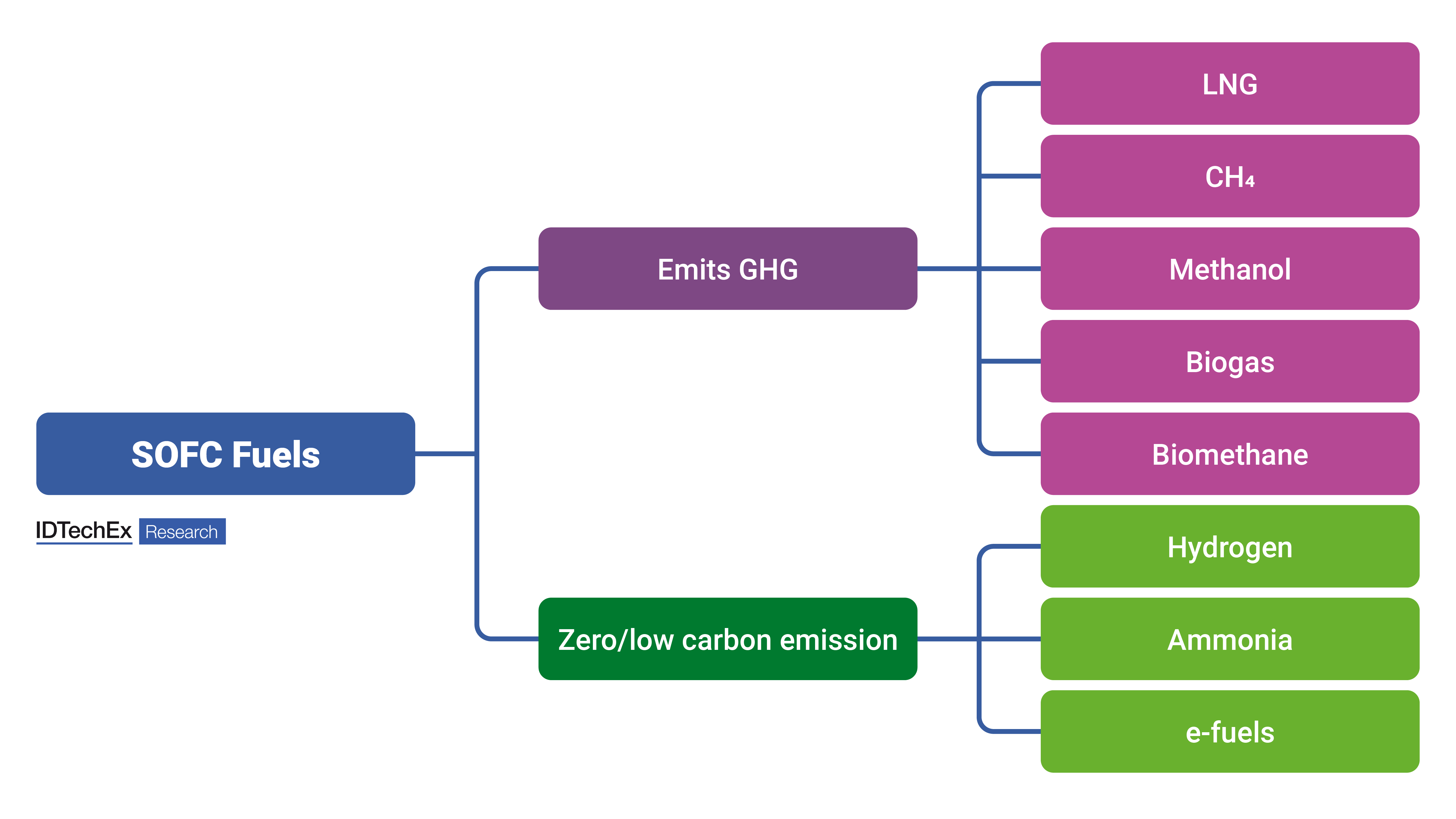

An overview of the main fuel choices for solid oxide fuel cells, segmented by carbon emissions. For further information on the solid oxide fuel cells market, see the IDTechEx report “Solid Oxide Fuel Cells 2023-2033: Technology, Applications and Market Forecasts”. Source: IDTechEx

While PEMFCs can only run on hydrogen, SOFCs can run on multiple fuels such as hydrogen, LNG, biogas, methanol, ammonia, e-fuels, and more. Liquefied natural gas (LNG) is the most deployed fuel in many applications, but it is not a long-term low-carbon solution due to methane slip and energy-intensive cooling and re-gassing processes. The utilization of methane (CH4) also produces both CO and CO2, while using methanol removes the emission of CO. However, despite the label of emitting greenhouse gases (GHG), reduction in emissions such as sulfur oxides, nitrous oxides, and organics can still be achieved with respect to coal-fuelled plants. Several fuels exist in the zero/low carbon emission sector, including hydrogen, ammonia, and e-fuels. The relative “green” nature of these fuels depends strongly on the source of the feedstock to produce the fuels – for example, green ammonia is primarily produced via green hydrogen.

There are major downsides with all the low-carbon frontrunners, which IDTechEx views as hydrogen, ammonia, and methane (natural gas) – with the use of methane in SOFCs considered low-carbon when compared with diesel combustion engines or coal-fired power plants. The key issue with hydrogen is its low volumetric energy density and storage temperatures of -263°C, which is energy intensive to reach and maintain. Ammonia does not require carbon capture but does require new bunker infrastructure and is highly toxic in a spillage. Green ammonia is a derivative of green hydrogen, so an abundance of green hydrogen must exist first. A byproduct of methane is carbon, meaning carbon capture is required for zero emissions, and this can be problematic due to added cost and complexity. Methane is the primary ingredient of LNG, the most deployed alternative fuel with decades of infrastructure. Methane is also susceptible to methane slip (boil-off methane), a powerful greenhouse gas, while ‘e-methane’ relies on carbon predominantly from industrial sources, which must ultimately be phased out.

An interesting case study can be examined for SOFCs for marine applications. Over the past year, a trend has emerged amongst companies producing larger-scale stationary power solutions to look towards the marine sector. For example, Bloom Energy and Ceres Power have formed partnerships or announced pilot projects to explore the marine sector, and Alma Clean Power is focusing solely on marine, developing an ammonia-powered system. Both ammonia and methane are widely transported by the sea today. In contrast, hydrogen is not, giving a competitive advantage for the use of ammonia and methane in the marine sector. At the same time, the former is preferred over the latter due to the lack of emissions produced when using ammonia in a SOFC.

In a future centered around the hyped hydrogen economy, PEMFCs should be expected to dominate the fuel cell market. However, SOFCs offer interesting opportunities in the interim while operating on today’s widely available fuels and pipeline infrastructure. An assessment by IDTechEx of almost 30 SOFCs from a range of suppliers that are commercially available (or near launch) showcases the fuel flexibility of the solid oxide fuel cell. This fuel flexibility, namely the ability to operate on the fuel choices for both today and tomorrow, sees SOFCs being positioned as a technology to enable a transition in power production methods – while also unlocking the ability for zero-emission power generation using fuels such as ammonia.

For more details on the SOFC technology, market trends, and key and emerging players, please see the IDTechEx market report “Solid Oxide Fuel Cells 2023-2033: Technology, Applications and Market Forecasts“.