Captain Alavi is a shipping industry veteran of 51 years and his experience encompass the full spectrum of the industry. During his professional career in addition to being a shipowner and ship operator, he has had a considerable number leadership role at a diverse range of maritime organization.

Captain Alavi is a shipping industry veteran of 51 years and his experience encompass the full spectrum of the industry. During his professional career in addition to being a shipowner and ship operator, he has had a considerable number leadership role at a diverse range of maritime organization.

In this opinion piece Saleem Alavi raises the question whether all shipowners should be expected to pay for technology firms’ decarbonisation R&D. His premise is that the proposals for a research fund by the leading shipowner associations and larger shipowners is being pushed on the industry without them having a say on the matter.

The personal opinions expressed in this article are those of Captain Alavi and do not necessarily reflect those of the organisations he is associated with nor of this publication.

He can be contacted at mail.salavi@gmail.com

The shipowner is a proverbial scapegoat in today’s environmental perspective.

For those who are not familiar with the definition of a scapegoat “a goat sent into the wilderness after the chief priest had symbolically laid the sins of the people upon it (Lev. 16).” I have written this article because I strongly feel that the shipowner is pushed for compliance with regulations without being given sufficient time to adapt to compliance practically. Today I will limit my discourse to the demand by the “acronym soap of representative bodies” or as I refer to them – the Umbrella Organizations representing countries’ shipowners’ organizations.

The proposal is put forward to MEPC ( 75/7/4. 18 November 2019) by Bimco, International Chamber of Shipping (ICS), InterCargo, Interferry, InterTanko, International Product Tanker Association (IPTA) – all Europe based, World Shipping Council and CLIA, based in Washington, DC. – collectively representing some 90% of the world merchant fleet across all trades and sectors. These organizations are joined by 5 European nations (Denmark, Greece, Georgia, Malta, Switzerland) and 2 Asian (Singapore, Japan), 2 African (Liberia, Nigeria), and 1 Micronesian (Palau – US compact country). We all know and accept, these are well reputed and respected bodies who are supposed to protect the shipowner’s interest, but in reality do they?

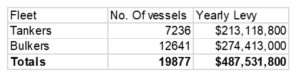

These well-known shipowner umbrella organizations have joined together to present a proposal that each vessel over a certain threshold will be subjected to this mandatory levy of $2.00 per ton of fuel used on yearly basis for shipping decarbonisation research. This mandatory levy on shipowners is supposed to raise USD5 billion over 10 years at $500million per year. Under this scheme, I estimate over 40,000 existing vessels will be forced to pay this mandatory levy. I did a fast analysis on two main sectors of shipping Tankers and Bulk Carriers ONLY the table as below: the amount of funds that will be generated yearly and if you add the additional 20000 or vessels it will be more or less close to a billion dollars.

How well acquainted are these umbrella organizations are to the prevailing market conditions about the earnings capabilities of various sectors/segments of shipping? Various industry report reflects that the 2021 average yearly VLCC’s earnings are close to $3000 or for the panamax tanker (dirty) is close to $4500 per day. Do they ever analyze how the shipowners will be able to come up with the money in depressed markets?

Everyone in the shipping industry is well acquainted that the shipping industry standard experience is estimated at 2-3 years of boom and 3-4 years of bust with few short blips of high earnings in between? I don’t deny the need to address the emissions from the shipping industry, but this needs to be done with a realistic approach without killing the industry.

Ships, with few exceptions, are supposed to have an average earning age of 20 years. So to meet and comply with new applicable regulations, it is simply not possible for a shipowner to convert the ship if the conversion costs cannot be paid back within the earning life that is left. No financial institution will be willing to finance conversion costs because of payback time and market conditions.

For example, the 2020 regulation regarding Sulphur Cap. The IMO resolution called for a review of the 2020 deadline in 2018, instead IMO decided to advance the decision review deadline to 2016 and confirmed the 2020 applicability deadline. The majority of the shipowners were left with only one option to use blended low sulfur fuel. There are numerous issues, both commercial and technical, with the use of this type of fuel are currently being experienced by the shipowners. The market conditions and the earning age of the ships should be taken into considerations when asking the shipowners to make alterations to comply with new regulations.

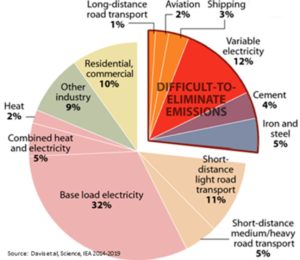

There has been constant unabated media coverage about emissions from the shipping industry, an industry that as part of the transport sector has less than 2.7% of CO2 emissions globally against 1.9% from Aviation and 11.9% of Road Transport. The media hype that’s is constantly berating the shipping industry for its GHG/CO2 emissions in electronic and print but hardly go heavy against the biggest anthropogenic emitters the “utilities 32%” or in the transport sector the “the road transport (11.9%)”. Because of the prevailing high gas prices, the Utilities mainly in Europe, Japan, India, China have conveniently switched to coal-fired plants to take advantage of pricing without media noticing it or talking much about it. Such a switch facility is not available to the shipowner to take advantage of pricing or due to shortage because it is illegal to carry HFO/IFO.

Research Funding

The basic premise of the fuel levy proposal by the shipowner’s umbrella organization is that the funds are needed for R&D research. Once again my question to these umbrella associations is “are you aware of how many waterborne projects have been researched for de-carbonization to date?”

In 2016 post COP21, 23 countries, and the European Union, led by the United States, joined Mission Innovation (MI)to “accelerate the pace of clean energy innovation.” In recognition of the need for greater investment, MI members committed to double the clean energy RD&D funding within 5 years from a baseline of $15 billion in 2016 to $30 billion by 2021. (https://itif.org). This RD&D clean energy focus but does include the clean fuels.

RD&D related to waterborne transportation: since COP21 (2015) there are numerous RD&D projects on CO2 reduction/CCUS done by EU, OECD countries, UN bodies, IEA, EIA, etc., plus many reputed institutes like Chalmers, Delft, UMAS, etc., to name the few.

In May 2021 ECSA-ICS released a report “FuelEU Maritime – Avoiding Unintended Consequences”. This ECSA-ICS report does not mention an earlier report regarding decarbonisation R&D about waterborne transport released by TRIMIS on March 24th, 2021 – (“Waterborne transport in Europe – the role of Research and Innovation in decarbonisation”). This report provides an overview of relevant European Research and Innovation (R&I) projects dealing with waterborne transport decarbonisation, based on the European Commission’s Transport Research and Innovation Monitoring and Information System(TRIMIS).

The report presents an analysis of Research and Innovation (R&I) projects in the field of waterborne transport decarbonisation in Europe since 2008. It identifies how technological, operational and coordination, and support measures could contribute to the target of carbon neutrality in the European Union (EU) including the waterborne sector.

The projects analyzed are from the Transport Research and Innovation Monitoring and Information System (TRIMIS) database, which is an open-access searchable database containing nearly 8,000 projects and programs financed by the EU Research Framework Programs such as FP7 and Horizon 2020 (H2020), but also other programs such as CEF, the environment and climate-focused LIFE program and some funded through other routes (such as the EU Member States and other countries.

Spending on waterborne transport decarbonisation research under FP7 and H2020 increased within 2012 and 2018, which are related to the concluding activities from the two framework programs. Moreover, the percentage of decarbonisation projects related to waterborne transport changes substantially in H2020, with a great increase in the budget allocated to these projects and reflecting increased attention within EU policies towards decarbonisation.”

“Under the 7th Framework Program (FP7) and Horizon 2020 (H2020) around €995 million has been invested in waterborne transport decarbonisation research projects. This includes €760 million of EU funds and about €239 million of own contributions by beneficiary organizations.

My question here is if so many programs related to waterborne transport are already funded and researched does these shipowners associations umbrella organizations know what programs are they expecting to research?

Conclusion

Although shipping has a very small GHG footprint compared to other sectors of the transportation industry as well as on an overall basis when compared to other industries, is the most heavily regulated industry, and lately, the implementation of these regulations windows are very narrow.

Shipowners have been very easy to push to comply with new regulations as there is practically no one to stand and defend them logically and with facts in a convincing way in the chambers where their fate is decided.

I agree with Mark O’Neil’s contention that “Shipping needs a unified voice, not an incoherent squeak”. My advice to the shipowners regarding carbon trading instruments, kindly do check how this scheme will benefit the environment, if any. Topic for another day.