While the shipping industry debates hydrogen’s role in the maritime energy transition, a report from the International Energy Agency (IEA) indicates that the fuel will be close to the market regardless of whether ships use it or hydrogen-based fuels. Two of four areas for development in the document – prepared for the G20 meeting of environment ministers in Tokoyo in June – involve maritime businesses.

The report, ‘The Future of Hydrogen’, explores the steps needed to develop a viable global hydrogen fuel market. Among these, IEA recommends making industrial ports the nerve centres for scaling up the use of clean hydrogen, as well as launching the hydrogen trade’s first international shipping routes.

Much of the refining and chemicals production that already uses hydrogen derived from fossil fuels is already concentrated in coastal industrial zones, including the North Sea, the US Gulf Coast and southeastern China. IEA argues that encouraging these plants to shift to cleaner hydrogen production would drive down the currently prohibitive costs associated with carbon-neutral hydrogen. These large sources could then also fuel ships and trucks serving the ports and power other local industrial facilities.

The report also acknowledges that, if clean hydrogen is to make an impact on the energy mix at a global level, an international hydrogen trade is a pre-requisite. The authors of the report therefore suggest that hydrogen stakeholders draw lessons from the successful growth of the LNG market, in particular by establishing the first international shipping routes for the hydrogen trade.

As well as driving the global market in hydrogen, both measures could also help to make hydrogen or hydrogen-derived fuels more competitive for shipping. IEA estimates that hydrogen bunkering infrastructure could be 30% more expensive than that required for LNG, even without the prerequisite development of the hydrogen supply network.

The main cost components for hydrogen bunkering are identified as storage and bunker vessels. On-site or nearby hydrogen would be needed for small ports given smaller flows and the high cost of dedicated hydrogen pipelines.

“Due to the cost of liquefying and high storage costs, hydrogen is likely to be more costly than other low-carbon alternatives for long-distance maritime transport,” the study notes.

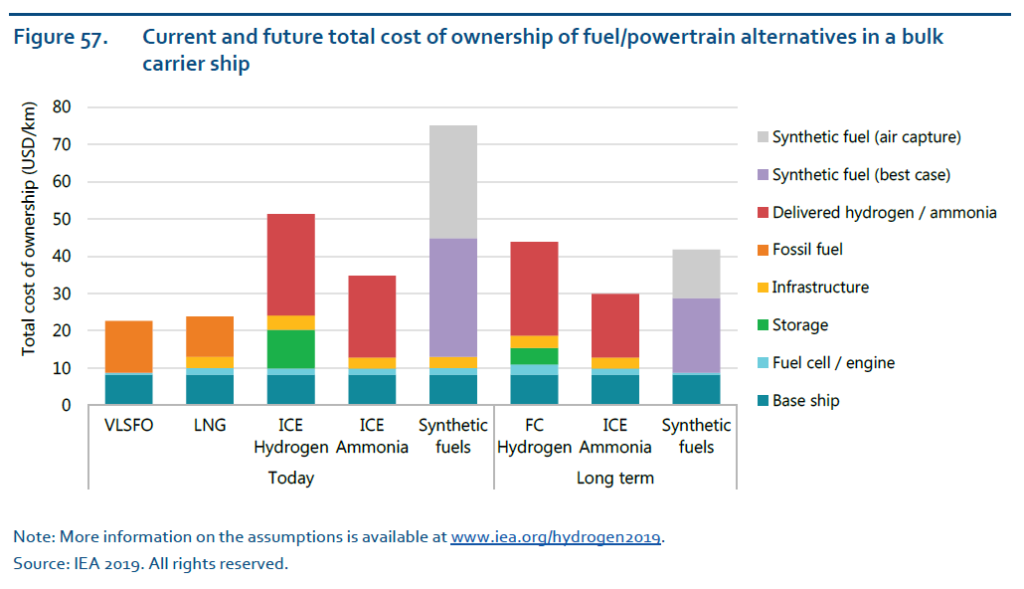

Big advances are also needed to make hydrogen-derived fuels like ammonia competitive, the report noted. Satisfying shipping demand in the long term would require 500 Mt of ammonia – almost three times the level of current global production and around thirty times the volume of ammonia currently traded. Cost is also an issue. The authors calculate that for a typical bulk carrier, policies equivalent to a carbon price of US$40–230/tonne (depending on electricity and fuel prices) would be needed to make engines running on ammonia competitive with fuel oil.

Regardless of its use or not as a marine fuel, port hubs and international trades would enable shipping to benefit from an expanding hydrogen market. Governments should also leverage existing gas infrastructure and support uptake of fuel-cell vehicles, IEA argues. The report concludes: “By building on current policies, infrastructure and skills, these mutually supportive opportunities can help to scale up infrastructure development, enhance investor confidence and lower costs.”

Details of the report can be found on the IEA website here