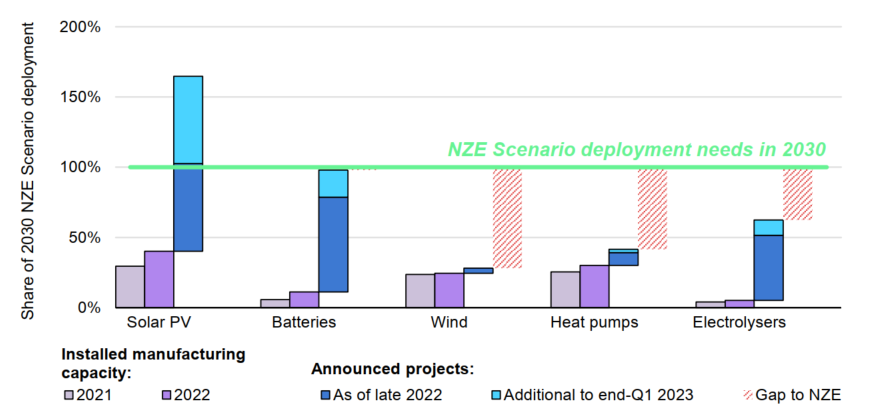

The International Energy Agency (IEA) has identified significant gaps in the production capacity for wind energy and electrolyser equipment, both critical for the scaling up of renewable e-fuels. In a report prepared for the G7 Leaders Summit in Hiroshima the agency noted that, unlike three other clean technologies investigated, announced projects for wind and electrolyser production currently fall well short of delivering the energy capacity needed by to meet IEA’s 2030 scenarios for net-zero emissions by 2050.

Electricity from wind turbines is one of the key feedstocks into renewable fuels, while electrolysers would use that electricity to produce green hydrogen, which can further be processed into green ammonia, methanol or e-diesel. As a result, production capacity of both wind and electrolyser technologies will have a direct impact on the availability of green fuels to the maritime market.

Manufacturing capacity for wind technology grew modestly in 2022, at around 2%. IEA noted that projected throughput from existing capacity and announced projects for wind technology would equate to just under 30% of the deployment levels needed to achieve the IEA’s Net Zero Emissions by 2050 (NZE) Scenario in 2030. However, lead times for constructing these facilities can be relatively short, around 1-3 years, “implying a more positive outlook than the gap initially suggests”.

Electrolyser manufacturing capacity grew from around 8GW in 2021 to 11GW in 2022, with announced projects to the end of Q1 2023 suggesting that nearly 125 GW of additional installed manufacturing capacity could be expected by 2030. That would achieve more than 60% of the levels needed in the NZE Scenario in 2030, but counting only committed projects, the figure drops to under 10%.

technologies in 2030 in the Net Zero Emissions by 2050 Scenario (source: IEA)

While the projections reveal potentially scarce electrolyser capacity, they also highlight the impact of scaling up on green fuel costs – if all planned projects were realised, costs for electrolysers could fall by more than 60% by 2030.

The outlook is more positive for batteries, which could also play a defining role in maritime decarbonisation on coastal and short-sea vessels and in reducing fuel consumption on larger vessels. Battery manufacturing throughput stood at 340 GWh in 2021 and reached 660 GWh in 2022, with around 90% of new battery projects destined for automotive applications. IEA’s assessment puts the total projected output from existing and announced projects at just below the levels required by 2030, around 5.9 TWh annually.

However there is still a need for supporting projects through to the final investment decision; if only committed projects materialise, there would be a 50% gap in capacity needed by 2030.

At the G7 summit, the leaders identified clean energy technology supply chains as a concern. The IEA report bears this out. Four countries and the European Union account for around 80-90% of global manufacturing capacity for the five clean technologies examined. China alone accounts for 40-80%, although it all announced projects were to be realised, these shares would shift to 70-95% and 30-80% respectively.

The report noted: “Major policy announcements of the past year are already starting to diversify supply chains, as evidenced by the scale-up in planned battery manufacturing capacity in the US following adoption of the Inflation Reduction Act.”